What can Healthtech learn from Fintech?

Venture capital funding in the Fintech space has skyrocketed globally over the last decade, it has transformed nearly every aspect of traditional banking and has driven broad-based access to financial products, and services to the unbanked and also underbanked by making financial services more streamlined and accessible.

Now, looking at those lessons learned and applying those to another longstanding critical sector that is stuck in industry inefficiencies paired with a lack of innovation, affordability, and poor consumer experience - the healthcare sector. Healthtech is a great example of trying to disrupt another public sector given its fertile ground for innovation and streamlining it.

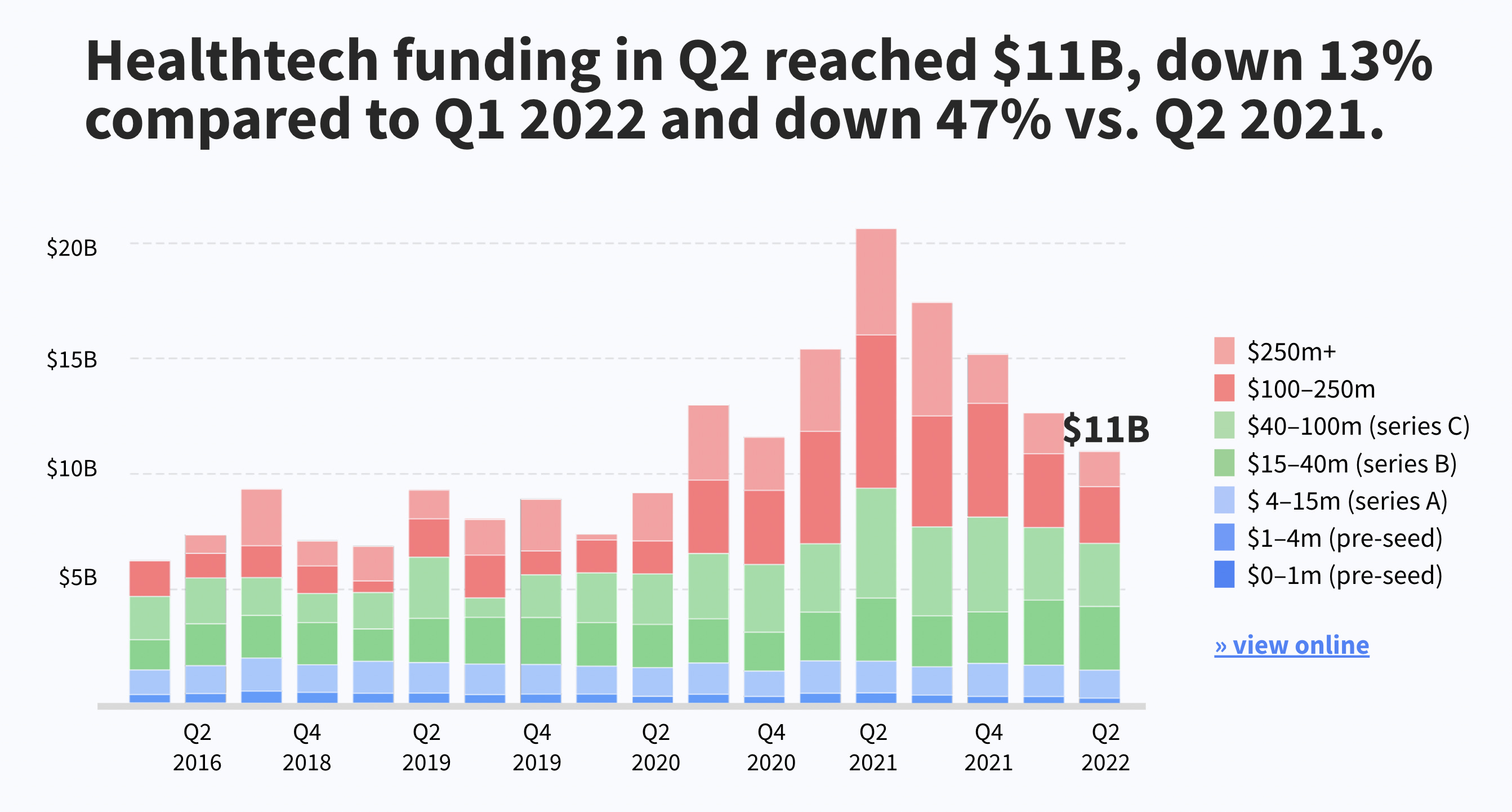

However, even though healthcare has failed to keep pace, the pandemic has also demonstrated how technology & innovation could drive a large transformation of the healthcare system. This is underlined by the restarted frequencies from a flat sinus rhythm in form of venture capital funding in the past year. The sector has seen a massive increase in venture funding, innovation, and new entrants from the TMT sector and large players such as Amazon with their increased M&A activities in this field. After a record year for healthtech startups in 2021, raising globally ~$44bn, an additional ~$24bn has been raised throughout the first half of 2022, with more to expect.

Digital transformation in healthcare is about far more than simply scheduling an appointment with a clinic, or getting their first assessment through a video call. It is also about empowering a new form of care, by erasing a large chunk of friction for patients to improve efficiency and most importantly the quality of care.

The digital disruption of the banking industry offers helpful comparisons and takeaways for the future of healthcare and healthcare finance. Banking has continued to innovate over the past decade, taking inspiration from adjacent industries as well as the biggest players in tech, growing as an ecosystem while staying oriented around customers’ needs. But what to start with? I believe, it needs a stronger focus on building an ecosystem around care, leveraging the created data, while simultaneously building a strong data aggregation infrastructure.

🏋🏼 Drawing the line between Fintech and Healthtech

The demands of the pandemic have required more speed and efficiency from healthcare organizations, acting as a tipping point for digital services, including payments and telehealth. The digital evolution of healthcare accelerated by the pandemic will continue as already strongly seen by the magnitude of venture capital flowing into this sector (see graph above), even in the current macro environment. But what will the path forward look like? My hypothesis is, that digitally enabled care will be the heart of the digital evolution as well as solving financial pain points in the convoluted process of paying for healthcare namely getting a hold on DRG reimbursement structures vs. out-of-pocket (”OOP”) expenses.

This transformation starts by erasing all sources of friction from the first point of contact with the patient (consumer), towards digitization of the whole value chain towards payment and post-treatment engagement.

❤️🩹 Digital-enabled care at the heart of the transformation toward digital healthcare ecosystems

One of the largest sub-sectors within the healthcare sector is in-hospital services, which are screaming to be part of the digital healthcare transformation and present opportunities for a greater shift. But one step back, what is the current shape of in-hospital services?

Chronic under-investment in the healthcare sector across Europe mismanagement over decades and the pandemic had pushed it past its limits leading to a staff retention and bed capacity crisis, hence constraining the provision of care.

But how can this even happen in the European Union, a union consisting of 27 European countries and a yearly budget of ~€165bn (2022)?

It is driven by the small magnitude of growth of healthcare expenditures in the European Union, since 2014 healthcare expenditures have only grown by ~3.4% (CAGR) compared to Industry 4.0, or the Financial Sector where expenditures grew double digits per annum.

Healthcare systems are organized and financed in different ways across the EU Member States, but universal access to quality healthcare, at an affordable cost to both individuals and society at large, is widely regarded as a basic need; moreover, this is one of the common values and principles of EU health systems.

Now, increasing hospital cases and demand for hospital beds since November 2019 across Europe, have led to an imbalance of supply & demand within the hospital structures leading to an “overcrowding effect” and some could even go so far and saying we see a “bullwhip effect” (usually used in a supply chain context) due to the imbalance supply & demand structure of beds vs. healthcare staff.

Emphasizes longstanding industry inefficiencies which led to affordability, outcome, quality challenges, and poor consumer experience. These inefficiencies are not new and provide the fertile ground for innovation to deliver high returns. It is one of the major challenges of the healthcare system which is now tackled by a variety of players who are trying to make care more accessible, effective, sustainable, and most importantly resilient.

Nevertheless, I would like to see those players thinking a couple of steps ahead, and see what players like Klarna, and Revolut have done to capture and improve customer experience along their value chain. They have been driving their industry transformation through the creation of their ecosystem.

Ecosystems create powerful forces that can reshape and disrupt industries as we have seen. In healthcare, they have the potential to deliver a personalized and integrated experience to consumers, enhance provider efficiency as well as improve quality and affordability.

Ecosystems have emerged across the financial industries because they:

Address industry inefficiencies, by optimizing underutilized assets

Create network effects, magnitude results in value

Leverage data generated in the ecosystem

Own scarce supply (healthcare staff)

Applying this framework to the healthcare sector, my perspective is, that the healthcare ecosystems of the future, will be centered on the consumer, around care in the first instance. The capabilities and services that form the healthcare ecosystems of the future will include but are not limited to:

Reinvention and digitalization of traditional care (i.e direct care)

Technologically enabled home and self-care - patient engagement, self- and virtual care, remote monitoring, and traditional care that can increasingly be delivered near or in the home (i.e. virtual ward)

Social care through social and community networks related to a patient’s holistic health focused on community elements of unmet social needs

Patient actions and habits enabling wellness and health, including fitness and nutrition

Financing support for operations and financial infrastructure supporting industry care events, including payment and financing solutions

The consumer-oriented nature of these ecosystems also will increase the number of healthcare touchpoints, modify patient behavior, and improve outcomes similar to what we have seen in the past with Revolut building their product consumer-centric and transforming the financial sector. Due to the similarities of the consumer / patient journey, it is inherent to start with care as the heart of the transformation. An additional point, which was so far neglected is data. The ecosystem infrastructure backbone also enables seamless data capture and aggregation to maintain data integrity and enable analytical insights (More to come below).

Luckily, we see already a lot of strong companies in Europe tackling either the whole ecosystem approach or taking on some of the cornerstones, which is highly needed. In this regard, I am super excited to share some news with you tomorrow 🚀, but until then stay tuned 🤝

🪢 Data aggregation, liquidity, and sharing

When it comes to data processing, the healthcare sector is still stuck in the early 2010s, which is another evidence of the incapacity of the authorities. There are three parts to healthcare's data problem: access/liquidity, processing, and insights, driven by the disparate healthcare landscape and operational silos as well as stringent industry regulations on how data is handled, by the authorities and the European Union.

Data liquidity—the ability to access, ingest, and manipulate standardized data sets—is required for the infrastructure layer to serve as the foundation for all insights and decisions made in the ecosystem. This data liquidity enables the ecosystem to create value and removes silos by allowing stakeholders to operate off the same data sets with increased coordination - similar to what we have seen back in the day with SWIFT or IBAN messaging systems to transmit financial data. Increased data liquidity enables stakeholders to access a complete longitudinal patient record, consisting of patient-generated data, provider-generated data, health and wellness data, financial data, and social data. As standards are established and cloud services continue to proliferate, this data will be easier to consume and integrate, but also to access (through data sharing).

In fintech Data sharing was accelerated and largely enabled by the introduction of PSD2 (Payment Services Directive 2) which is arguably one of the main drivers for open banking, which supports the sharing of payment account data between banks and other payment services providers (PSPs), to drive innovation in banking and payment infrastructure, enabling banks as well as PSPs to share data more easily (Securely) between each other, empowering a stronger UX. A couple of years, the healthcare sector started also to democratize access to information which should ultimately lead to greater transparency and flexibility in how services are delivered and supported. Local healthcare services providers such as NHS or Terveystalo support a personal health record app, to store patients’ health information in one place, or Kry, as one of my favorite examples of lean data storing principles. However, despite that innovation, medical records are majorly still stored in an obsolete manner as of day. Every physical practice or hospital stores physical files per patient, which makes accurate data aggregation and data sharing close to impossible. We surely need solutions for data aggregation cross-application (P2P).

⌚️ Let's focus on the timing, which is now

“It is not the strongest of the species that survives, nor the most intelligent, but the one most responsive to change.” - Charles Darwin

We have seen over the past decade that fintech’s innovation and tremendous impact made effortless and frictionless transactions the norm for billions of people, leveraging the regulatory structure, and not shying away from complexity. I believe now is the time that ambitious healthcare founders to take that momentum by adopting the same norms. Covid has surely amplified disparities in this field, which need to be counteracted and equalized again.

Consumer/patient demands and journeys, regulatory frameworks, and technological opportunities have the potential to usher in a new era in healthcare. Up until now, payers, providers, and consumers have traditionally occupied disparate—if not adversarial—roles.

See you in two weeks 🦄

PS: Feel free to share this post with whomever you think is helpful!